10 Must-Have Features in Insurance Policy Analysis Software in 2026

Summary

Insurance policy analysis software is the AI and automation layer that ingests submissions, extracts data from ACORD forms, loss runs, schedules, and broker emails, and feeds structured outputs into underwriting, pricing, and compliance workflows. For commercial P&C carriers, MGAs, brokers, and reinsurers, the ten features that separate production-grade platforms from demos in 2026 are:

- ACORD-native document extraction and submission intake

- Configurable underwriting rules engine with appetite logic

- Real-time predictive analytics and loss modeling

- Explainable AI with NAIC, NY DFS, and EU AI Act controls

- Deep PAS, CRM, and data-vendor integrations

- Cloud-native architecture with insurance-grade security

- Custom portfolio reporting and loss-development analytics

- Workflow automation for quote-to-bind, renewals, and endorsements

- Role-based UX for underwriters, brokers, and ops

- Transparent, usage-aligned pricing

What is insurance policy analysis software?

Insurance policy analysis software is an AI-driven system that automatically extracts, structures, compares, and reasons over insurance documents (submissions, ACORD forms, schedules, loss runs, quotes, bound policies, and endorsements) and routes the structured output into underwriting, claims, pricing, and audit workflows.

Modern platforms combine document AI, configurable rules, predictive models, and explainability controls designed to satisfy NAIC and state-level AI governance requirements.

"The winning systems will not be generic OCR wrappers. They will combine insurance-specific document intelligence, source-grounded policy comparison, deterministic validation, and human approval workflows that fit how carriers, MGAs, and brokers already operate.” — Ben Grosser, Head of Insurance AI at FurtherAI

1. ACORD-native document extraction and submission intake

Generic OCR fails on commercial submissions. A typical mid-market submission contains an ACORD 125, an ACORD 126 or 140, an SOV with hundreds of locations, three to five years of loss runs in different broker formats, and a free-text broker email with the actual ask. Production-grade policy analysis software is purpose-built for these document classes.

What to look for:

- Native parsing of ACORD 125, 126, 140, 25, and prior-carrier wordings, with field-level confidence scores

- Structured loss-run normalization across broker templates (Marsh, Aon, WTW, regional MGAs)

- Schedule-of-value parsing with TIV reconciliation and COPE attribute extraction

- Email and attachment triage that links the broker ask to the documents needed to underwrite it

2. Configurable underwriting rules engine with appetite logic

A configurable underwriting engine lets underwriting leaders codify appetite, refer-out triggers, and auto-decline criteria as data and not as tribal knowledge in senior underwriters’ heads. The result is fewer in-appetite declinations, less appetite drift across branches, and faster cycle time on the risks the carrier actually wants to write.

What to look for:

- Rule authoring by underwriting managers, not engineers

- Per-segment, per-line, and per-geography overrides

- Versioning, A/B testing, and shadow-mode evaluation before rules go live

- Audit logs that show why a submission was declined or referred

Look hard at how the engine handles ambiguity: real submissions are not clean enough for binary rules. Platforms that support graduated referral logic outperform pure pass/fail engines.

One of FurtherAI’s clients reported saving more than 2,000 hours of manual work by automating data extraction and enrichment tasks that were historically handled by underwriting assistance. In the first 3 months, this led to a 200% improvement in underwriting efficiency with over 99% accuracy rates.

3. Real-time predictive analytics and loss modeling

Predictive analytics turn historical claims data, third-party signals, and submission features into pricing, retention, and reserving decisions. The bar in 2026 is not whether the platform has models, but whether models are wired into the underwriter’s workflow at the moment of decision, with explainability that survives a market conduct exam.

Common model types worth evaluating:

- Loss-cost models for severity and frequency by class

- Premium leakage detection on bound policies

- Retention and lapse models for renewals

- Anomaly detection on claims and endorsements

Vendor benchmarks from 2024–2025 industry reviews continue to show Guidewire Analytics, Akur8, and SAS Viya leading on production-grade pricing models, while newer entrants compete on speed of model deployment and the quality of the underwriter-facing explanation layer.

4. Explainable AI with NAIC, NY DFS, and EU AI Act Controls

The regulatory environment for AI in insurance changed materially between 2023 and 2026. Software that cannot produce a reviewable, decision-level audit trail has essentially turned into a compliance liability.

Minimum compliance posture in 2026:

- NAIC Model Bulletin on the Use of AI Systems by Insurers (adopted December 2023): documented AI governance, written program, model risk management, third-party AI vendor oversight

- NY DFS Insurance Circular Letter No. 7 (2024): governance, risk management, and consumer-protection controls for AI and external consumer data

- Colorado SB21-169 and Regulation 10-1-1: testing for unfair discrimination in life-insurance algorithms and external data

- EU AI Act: pricing and risk-assessment AI in life and health insurance is high-risk, with conformity assessment, documentation, and human-oversight obligations

- SR 11-7-style model risk management for any pricing or reserving model

Practical features that satisfy these regimes: per-decision feature attribution, adverse-action explanations underwriters can actually read, sandbox environments for model testing, and exportable evidence packs for examinations.

5. Deep PAS, CRM, and data-vendor integrations

Policy analysis software does not replace a policy administration system; it sits in front of and alongside one. The integration surface is where most implementations stall.

Integration targets that matter:

- Policy administration systems: Guidewire PolicyCenter, Duck Creek Policy, Majesco, Insurity, Origami

- Broker and CRM systems: Salesforce Financial Services Cloud, Applied Epic, AMS360, Salesforce-based MGA stacks

- Data vendors: Verisk, LexisNexis, PitchBook, D&B, Moody’s RMS / KCC for cat exposure, sanctions and OFAC providers

- Communications layer: Outlook and Gmail for submission intake, e-signature, document management

Ask vendors for an API map, average implementation timeline by PAS, and references from carriers running the same PAS as you. Generic “open API” claims are not enough.

6. Cloud-native architecture with insurance-grade security

Cloud-native is now table stakes; insurance-grade security is the real bar. SOC 2 Type II and ISO 27001 are minimums. For carriers writing globally, GDPR, CCPA, and HIPAA controls (where applicable to health-adjacent lines) are required.

What to verify:

- Single-tenant or logical isolation options for sensitive book-of-business data

- BYO key management for cloud-stored documents

- Region pinning for EU and UK data

- Vendor model isolation — confirm whether your data is used to train shared models

- DPIA and AI conformity documentation for EU-regulated lines

7. Custom portfolio reporting and loss-development analytics

Reporting is where ops, finance, and reinsurance teams actually feel the platform. The right tool produces views that ladder up from per-policy data to portfolio-level loss development triangles, hit-ratio analytics, and reinsurance bordereaux without manual reconciliation.

What to require:

- Triangles, IBNR views, and incurred-versus-paid development at the portfolio and segment level

- Hit ratio, quote-to-bind, and bind-to-issue cycle-time dashboards

- Exposure-management views by class, geography, and cat zone

- Bordereaux exports compatible with reinsurer data-call standards (Lloyd’s MDC, treaty schedules)

- Self-service report builders for ops, with scheduled exports to reinsurers and brokers

8. Workflow automation for quote-to-bind, renewals, and endorsements

Automation features should target the workflows that absorb underwriting and ops capacity: quote-to-bind, renewals, mid-term endorsements, certificate issuance, and policy comparisons against prior-year wordings.

The renewal cycle is the single highest-ROI automation target for most commercial carriers and MGAs. A good platform should:

- Pre-populate renewal questionnaires from the bound policy and recent endorsements

- Compare the prior-year wording against the proposed renewal and surface material changes

- Auto-issue routine endorsements within rule-defined limits

- Flag expiring certificates and schedule client outreach

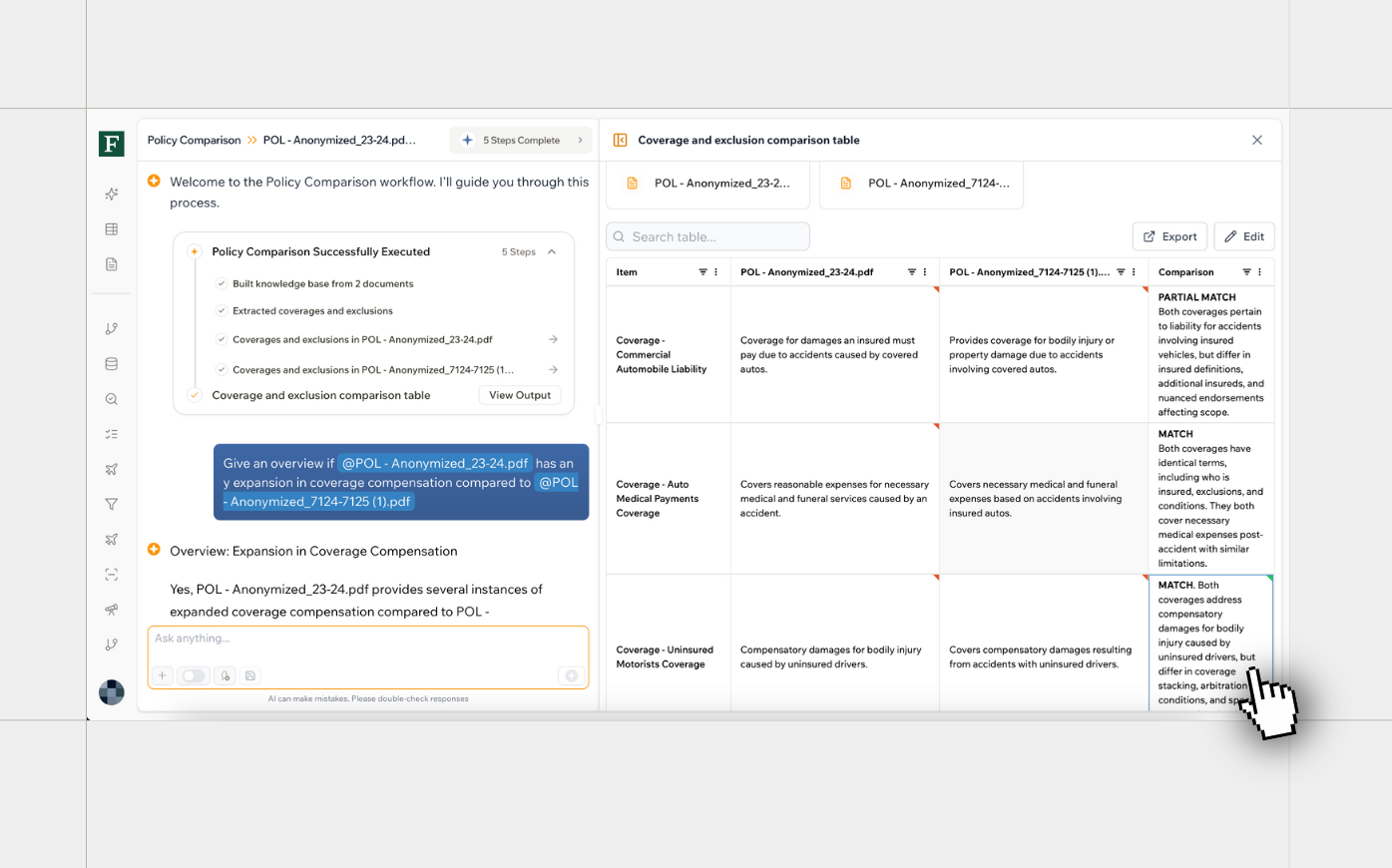

For brokers, the equivalent target is policy comparison across two or more carrier quotes — an exercise still done in spreadsheets at most retail and wholesale brokerages.

One of FurtherAI’s clients achieved a 30x faster policy comparison after introducing AI automation workflows. Combined with 20x faster policy checks and overall 95% operational efficiency gain, the company reported a 400% ROI within months of implementation.

9. Role-based UX for underwriters, brokers, and ops

Adoption is the killer of insurance software deployments. The platform an underwriter actually uses every day looks very different from the one a broker or an ops manager uses. So role-based UX is not cosmetic, but essential.

What to validate in the demo:

- Underwriter workspace that consolidates the submission, prior policy, loss runs, and rules-engine output on one screen

- Broker view that supports submission packaging and multi-carrier comparison

- Ops view for queue management, exception handling, and SLA tracking

- Mobile or tablet-friendly views for field underwriters and risk engineers

Adoption metrics to ask for include weekly active underwriters, average submissions touched per underwriter, and the percentage of submissions that route through the platform versus around it.

"After evaluating several vendors, we chose FurtherAI for its performance, insurance expertise, and partnership approach. The forward deployed engineer model makes a big difference — they work directly with our teams and help us get results quickly and we are able to both learn and iterate." — Doug Alexander, VP of Digital Delivery at Upland Capital Group

10. Transparent, usage-aligned pricing

Per-user pricing was built for agency management systems, not for AI-driven analysis platforms. In 2026 the pricing models that align cost to value are usage-based ( per submission, per policy, per document) with enterprise tiers that bundle volume.

Questions to ask vendors:

- What is the unit of pricing — user, submission, policy, document, or page?

- What is the three-year total cost of ownership including services, integrations, and model retraining?

- Are explainability, audit logs, and reporting included or charged separately?

- What support, SLAs, and customer-success resources are included?

Mid-market agency systems still cluster around $150–$200 per user per month at the mid-to-high tier, but carrier and MGA deployments at scale should be benchmarked against per-submission economics.

Comparison: Insurance Policy Analysis Platforms in 2026

Buyers typically evaluate FurtherAI alongside three classes of vendors: full PAS providers (Guidewire, Duck Creek), document-AI specialists (Indico, Cytora), and pricing or process-automation point solutions (Akur8, Roots Automation). Each occupies a different position in the stack.

Note: positioning above reflects publicly available product descriptions and FurtherAI’s evaluation framework as of May 2026. Confirm current capabilities directly with each vendor.

Regulatory considerations: NAIC, NY DFS, Colorado, and the EU AI Act

Three regulatory developments should shape the way buyers evaluate insurance policy analysis software in 2026.

The NAIC Model Bulletin on the Use of AI Systems by Insurers, adopted in December 2023. By early 2026, over half of all states had adopted the bulletin or substantially similar guidance.

It requires insurers to maintain a written AI governance program covering board oversight, model risk management, third-party AI vendor governance, testing for unfair discrimination, and ongoing monitoring. Buyers should expect AI vendors to provide documentation that maps directly to the bulletin's core program components.

NY DFS Insurance Circular Letter No. 7 (2024) is among the most prescriptive state-level guidance to date. It addresses the use of AI and external consumer data sources in underwriting and pricing, with explicit expectations on governance, risk management, and consumer-protection controls. New York-licensed insurers and any vendor selling to them should be able to produce evidence of conformity.

Colorado’s anti-discrimination regime, anchored by SB21-169 and Regulation 10-1-1, requires testing of life-insurance algorithms and external data for unfair discrimination, with detailed governance, testing, and documentation requirements; specific quantitative testing thresholds are pending in a separate draft regulation. Carriers writing in Colorado should treat the regulation as an early signal of the testing regime. Originally for life, it expanded in 2025 to private passenger auto and health benefit plans, with further P&C expansion expected.

The EU AI Act classifies AI systems used for insurance pricing and risk assessment in life and health as high-risk. High-risk classification triggers conformity assessment, technical documentation, post-market monitoring, and human-oversight obligations. US carriers writing through Lloyd’s, the London Market, or EU subsidiaries are advised to treat the Act as a binding requirement, not a future concern.

Build vs. buy: A decision framework

Mid-size and large carriers regularly evaluate building this capability internally. The honest answer is that the build path is justified only when three conditions hold simultaneously:

- The carrier has a stable in-house ML and document-AI team of at least 8–12 engineers with insurance domain experience.

- The book of business is concentrated in a small number of lines with stable document conventions.

- The carrier has 18–24 months of runway before the capability is competitively necessary.

For everyone else, including the majority of MGAs, brokers, and mid-market carriers, the buy path produces capability in months instead of years and offloads model risk management, regulatory documentation, and ongoing accuracy work to a vendor whose only product is this.

The high-leverage middle path is hybrid: buy the document-AI and rules-engine layer, build proprietary pricing models on top of structured outputs.

RFP checklist: 10 questions that separate vendors

Use these questions in vendor evaluation. The right answers are specific, not aspirational.

- What ACORD form versions and broker loss-run templates are natively supported, and what is the field-level extraction accuracy on a held-out test set?

- Provide three production references at insurers with a similar PAS, line of business, and submission volume.

- Which features are in-platform versus delivered through professional services? Quote both.

- Provide your AI governance documentation mapped to the NAIC Model Bulletin’s seven domains.

- Walk us through a per-decision explanation for a real declined or referred submission.

- What is the typical implementation timeline for our PAS, and which integrations are pre-built versus custom?

- How is our data isolated, and is it ever used to train models that benefit other customers?

- What is the unit of pricing, and what is the three-year TCO at our projected volume?

- What is your model retraining cadence, and how are model updates communicated and versioned?

- What is your roadmap for the lines and workflows we care about over the next 18 months?

How FurtherAI compares

FurtherAI is purpose-built for insurance policy analysis. The platform handles ACORD-native document extraction, underwriting audits, policy comparisons against quotes and endorsements, and end-to-end submission triage for carriers, MGAs, brokers, and reinsurers.

Where FurtherAI is differentiated

- Trained specifically on commercial P&C document classes — ACORD 125, 126, 140, prior-carrier wordings, broker emails, schedules, and loss runs

- Deep, prebuilt integrations into Salesforce, email, and data vendors (PitchBook, sanctions providers)

- Per-decision explainability and audit trails that map to NAIC Model Bulletin domains

- Usage-aligned pricing with measurable ROI in months, not years

“We had a producer spend hours trying to extract and format a loss run using general AI tools, and it just wasn’t working. When they ran the same file through FurtherAI, it produced exactly what they needed in minutes. That’s when it really clicked for us.” – Laurie Flanagan, Chief Project Officer at Leavitt Group

Frequently Asked Questions

Does insurance policy analysis software replace a policy administration system?

No. Policy analysis software sits alongside the PAS, not in place of it. It handles submission intake, document extraction, policy comparison, and underwriting analysis, then writes structured data into the PAS for binding, issuance, and policy lifecycle management. The right architecture treats the PAS as the system of record and the analysis platform as the intelligence layer above it.

Can it handle ACORD forms, loss runs, and broker emails out of the box?

Production-grade platforms parse ACORD 125, 126, 140, 25, and the major broker loss-run templates from Marsh, Aon, WTW, and regional brokers natively, with field-level confidence scores. Generic OCR and document AI tools require months of customization to reach the accuracy needed for commercial underwriting. Always evaluate on your real submissions, not the vendor’s curated demo set.

How is AI underwriting reconciled with NAIC explainability requirements?

The NAIC Model Bulletin requires a written AI governance program, documented model risk management, testing for unfair discrimination, and per-decision auditability. Reputable platforms produce per-feature attribution, adverse-action explanations, and exportable evidence packs that map to the bulletin’s seven domains. Buyers should ask vendors to walk through a real declined submission and show the audit trail end to end.

What is a realistic implementation timeline for a mid-size carrier or MGA?

For a focused use case (submission intake plus underwriting triage on one or two lines) production go-live in 8–14 weeks is achievable with a vendor that has prebuilt integrations to your PAS and CRM. Full enterprise rollouts spanning multiple lines, all renewal workflows, and reinsurance reporting typically run 6–12 months. Custom integrations into legacy PAS environments are the most common cause of slippage.

How does it differ from general-purpose document AI like Azure Document Intelligence or AWS Textract?

General-purpose document AI extracts text and form fields from any document. Insurance policy analysis software adds insurance-specific schemas, ACORD-native parsing, loss-run normalization, underwriting rules logic, regulatory-grade explainability, and integrations into PAS and CRM systems. Carriers using general-purpose tools alone routinely spend 12–18 months building the insurance layer that purpose-built vendors like FurtherAI deliver out of the box.

What KPIs should we measure to justify the investment?

Quote-to-bind cycle time, hit ratio, declination rate, premium leakage, expense ratio impact, underwriter capacity (submissions handled per FTE), and policy-comparison accuracy. The strongest business cases combine cycle-time gains with measurable expense ratio reduction and a quantified premium-leakage recovery.

Can brokers and MGAs use the same platform as carriers?

Yes, with role-specific UX and configuration. Brokers use the platform for submission packaging, multi-carrier policy comparison, and renewal questionnaires. MGAs use it for delegated authority underwriting, bordereaux production, and binder-to-policy reconciliation. Carriers use it for submission triage, underwriting, and portfolio analytics. The underlying document AI and rules engine are the same; the workflows and dashboards differ.

Is the data we feed into the platform used to train models for other customers?

Reputable insurance AI vendors operate strict tenant isolation and do not train shared models on customer data without explicit contractual permission. This question should be answered in writing in the master services agreement, with specific language on data isolation, model training, and termination data return.

The carriers, MGAs, and brokers compounding fastest in 2026 are not the ones with the largest tech budgets, but the ones who have moved policy analysis from a manual, document-shuffling exercise into a structured, AI-augmented workflow that respects the regulatory perimeter.

The ten features above are the difference between a platform that wins demos and a platform that earns its place in production. Evaluate against this list, validate on your own submissions, and demand evidence (not aspirations) from every vendor you consider.

DISCLAIMER

This article is for general informational purposes only and does not constitute legal, regulatory, compliance, underwriting, or other professional advice. The content reflects information available as of the date of publication, and FurtherAI undertakes no obligation to update it as laws, regulations, or AI technologies evolve.

Recent posts

.png)

Ready to Go Further &

Transform Your Insurance Ops?

Reclaim your time for strategic work and let our AI Assistant handle the busywork. Schedule a demo to see how you can achieve more, faster.

.svg)